Deserts look empty from far away. Economically, they are anything but empty. Many of the world’s driest landscapes sit above oil, natural gas, phosphate, copper, lithium, uranium, borates, salts, and other industrial minerals. Deserts cover about one-fifth of Earth’s land area and support around 1 billion people, so their value is not only underground. It also appears in export revenue, power generation, fertilizer supply, industrial chemistry, transport corridors, and local jobs.

That value comes from geology first. Dry air, sparse vegetation, exposed bedrock, closed basins, ancient seabeds, and long periods of evaporation all help create, preserve, or reveal useful deposits. In many desert belts, the rocks are visible, the stratigraphy is easier to map, and ore bodies stay less hidden than they do in wetter regions. Not every desert becomes rich. Yet when basin history, tectonics, and aridity line up, rich it can be.

| Desert Or Desert Belt | Main Resources | Concrete Data | Why It Matters |

|---|---|---|---|

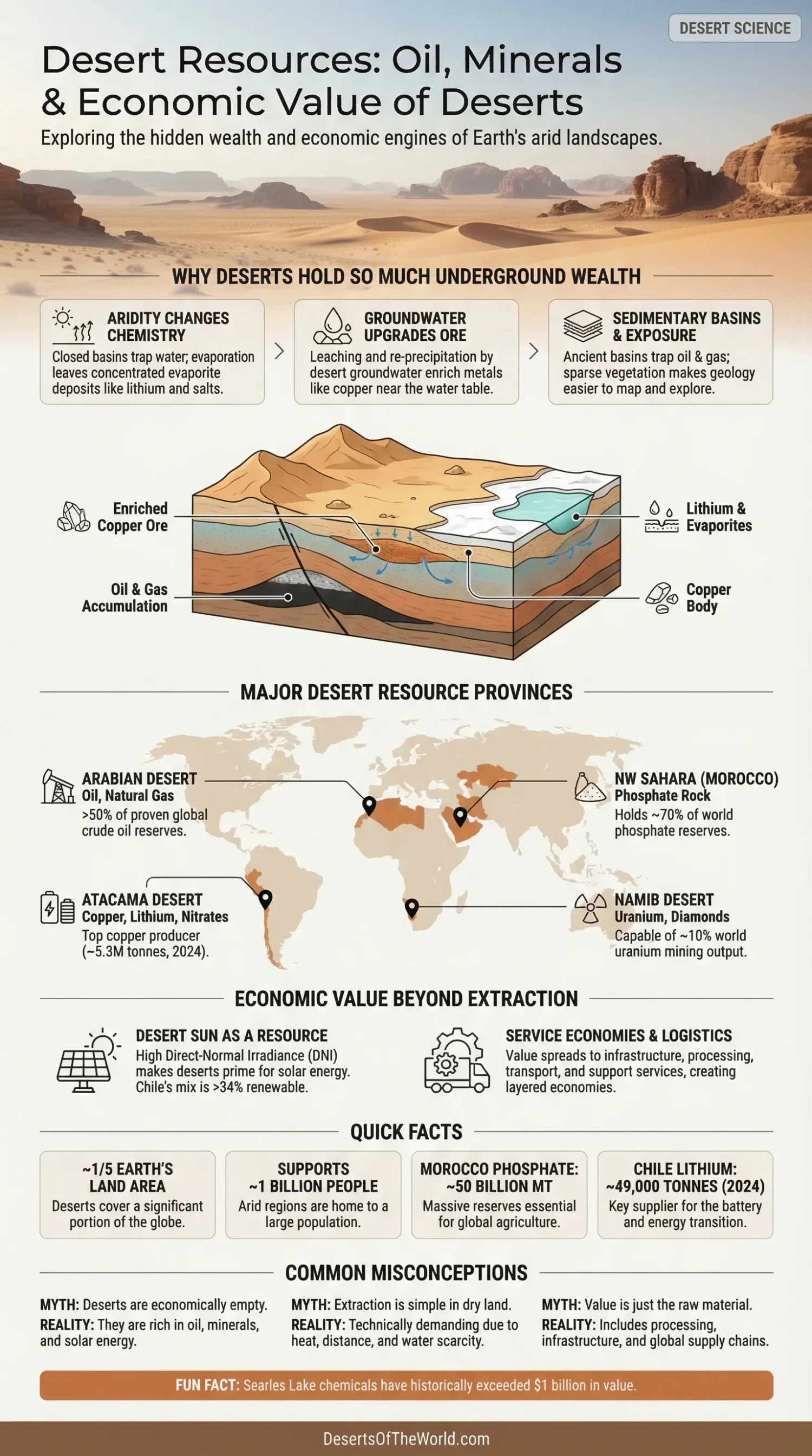

| Arabian Desert | Oil, natural gas, petrochemical feedstocks | World proved crude oil reserves stood at 1,567 billion barrels at the end of 2024; more than half of proven oil reserves lie beneath the Arabian Desert | Fuel exports, refining, petrochemicals, state revenue, industrial energy |

| Northwestern Sahara | Phosphate rock, oil and gas in nearby basins, salt, iron ore in wider Saharan zones | Morocco held about 50 billion metric tons of phosphate rock reserves, around 70% of world reserves | Fertilizer supply, export earnings, food production chains |

| Atacama Desert | Copper, lithium brines, nitrates, iodine, borates, solar resource | Chile produced about 5.3 million tonnes of copper and 49,000 tonnes of lithium in 2024; the hyperarid core receives less than 2 mm of rain per year | Power grids, batteries, chemicals, renewable energy, mining services |

| Namib Desert | Uranium, diamonds, lithium prospects, rare earth interest | Namibia produced 7,333 tonnes of uranium in 2024; Namibian uranium mines are capable of about 10% of world mining output | Nuclear fuel supply, exports, royalties, processing and port activity |

| Mojave And Great Basin Desert Systems | Borates, salts, soda ash, brines, industrial minerals | Chemicals produced from Searles Lake have historically exceeded $1 billion in value | Glass, detergents, ceramics, chemical manufacturing |

Why Deserts Hold So Much Underground Wealth

Aridity changes chemistry. In closed desert basins, water arrives, dissolves minerals, and then evaporates. What stays behind can become evaporite deposits: gypsum, halite, borates, nitrates, potash-bearing salts, and lithium-rich brines. A salt flat may look lifeless on the surface, yet below it sits a chemical archive built over thousands or millions of years.

Desert groundwater can upgrade ore. The U.S. Geological Survey notes that of the 15 major mineral deposit types in the Western Hemisphere formed by groundwater action, 13 occur in deserts. That matters for metals such as copper, where leaching and re-precipitation may enrich ore near the water table. Dry conditions also help preserve highly soluble minerals that wet climates would wash away.

Sedimentary basins matter just as much. Many hot deserts overlie thick sedimentary packages laid down in ancient marine or continental environments. Where organic-rich source rocks matured and migrated into traps, oil and gas accumulated. The Arabian Desert is the clearest example, but North African basins show the same broad logic.

Exposure helps discovery. Sparse soil and low vegetation leave outcrops open to mapping, sampling, and geophysics. Exploration still costs a lot, of course. Roads, drilling, water supply, and power lines do not build themselves. Still, a dry surface often makes the geology easier to read.

Oil and Gas in Desert Regions

Arabian Desert: The Best-Known Desert Hydrocarbon Province

The Arabian Desert is the clearest case where a desert landscape and a hydrocarbon economy meet. More than half of the world’s proven oil reserves lie beneath its sands, mainly under Saudi Arabia and nearby states of the Arabian Peninsula. This is not a random accident of dunes. It reflects thick sedimentary basins, long burial history, mature source rocks, structural traps, and large carbonate reservoir systems.

Oil value does not stop at the wellhead. It spreads through a chain: upstream drilling, gathering systems, pipelines, storage, refining, petrochemicals, ports, and shipping. A desert oilfield may be far from a city, yet it can anchor a whole industrial zone. Plastics, fuels, lubricants, solvents, and synthetic materials all begin with that buried carbon.

Natural gas adds another layer of value. Desert gas fields supply power plants, fertilizer plants, desalination systems, and export terminals. In dry countries, that link is especially visible: energy and water systems often move together. One supports the other.

Why Desert Hydrocarbon Projects Are Technically Demanding

Desert production looks simple on a map. On the ground, it is not. Heat strains equipment. Dust affects air intakes and rotating machinery. Distance raises transport costs. Water for drilling fluids, enhanced recovery, and camp use can be limited. The best desert fields work because logistics are solved early, not because the climate is easy.

Rarely does a desert petroleum project succeed on reservoir size alone. Surface infrastructure, maintenance access, export routes, and processing capacity decide whether a resource becomes long-term cash flow or just a line in a reserve table.

Mineral Wealth Beneath Arid Ground

Phosphate Across the Sahara Belt

Phosphate rock is one of the most economically important nonfuel resources linked to desert margins and arid basins. In northwestern Africa, Morocco holds about 50 billion metric tons of phosphate rock reserves, around 70% of world reserves. For agriculture, phosphorus has no real substitute. Crops need it. So do fertilizer producers.

This is why phosphate matters far beyond the desert itself. The chain runs from mine to beneficiation plant to phosphoric acid to DAP and MAP fertilizers to farms across multiple continents. A desert deposit in one country can influence food costs and fertilizer security half a world away.

There is also a technical side worth noting. Marketable phosphate is typically discussed in terms of P2O5 content. Ore has to be upgraded. Then it enters wet-process chemistry to produce phosphoric acid and finished fertilizer products. So the business is not only about extraction. It is about chemical processing, export handling, storage, and timing with global farm demand.

In Morocco, the mining sector accounted for 21.1% of total export value in 2020 and employed about 40,000 people. That shows the wider point clearly: a desert mineral resource becomes truly valuable when it supports a full industrial chain.

Copper, Lithium, and Nitrates in the Atacama Desert

The Atacama Desert in northern Chile is one of the driest places on Earth. Its hyperarid core receives less than 2 mm of precipitation per year. That dryness is not just a climate fact. It helps preserve evaporites, exposes mineralized systems, and shapes water use in mining. The Atacama is a mining desert in the most literal sense.

Chile produced about 5.3 million tonnes of copper in 2024 and held about 190 million tonnes of copper reserves. It also produced about 49,000 tonnes of lithium and held around 9.3 million tonnes of lithium reserves. Those numbers explain why the Atacama sits at the center of modern supply chains for power cables, motors, transformers, batteries, and energy storage.

The geology is varied. Porphyry copper systems dominate many mining districts. Salar brines support lithium extraction. Historic nitrate fields formed under intense aridity and evaporation. In practice, the Atacama is not one resource story. It is several stories stacked on the same dry landscape.

Chile’s wider energy system adds another layer. The International Energy Agency notes that Chile has around one-fifth of global lithium supply and almost one-quarter of global copper supply, while the Atacama has some of the world’s highest solar irradiance levels. That pairing matters. Mines need power. Desert solar can help provide it.

A useful detail often missed in short articles: desert mining value depends on water as much as grade. Brines must be pumped and later seperated into saleable compounds. Copper ores need crushing, flotation, leaching, or smelting routes. In a place as dry as the Atacama, water sourcing, recycling, and desalination can shape project economics almost as much as the orebody itself.

Uranium and Diamonds in the Namib Desert

The Namib Desert shows a different desert pattern. Its fame comes from diamonds and uranium. Namibia produced 7,333 tonnes of uranium in 2024, and the World Nuclear Association states that Namibian uranium mines are capable of providing about 10% of world mining output. That is a large share for a country with a relatively small population.

Much of the Namib’s uranium is linked to granitic and calcrete-hosted systems near the coast and inland desert belt. Calcrete deposits are especially tied to arid conditions, where groundwater movement and evaporation concentrate minerals in near-surface horizons. Dry climate is not just background scenery here. It is part of the deposit story.

Diamonds tell another story. In Namibia, many of the most valuable stones occur in coastal and offshore placer systems fed by ancient river transport and then reworked by marine processes. Desert plus coast. A rare combination, and a very profitable one when geology cooperates.

Borates, Salts, and Other Industrial Minerals

Not all desert wealth comes from headline commodities. Some of the steadiest desert value comes from industrial minerals. Playas and dry lakes can host borates, bromine-bearing brines, soda ash, sodium sulfate, halite, gypsum, and other feedstocks for glass, detergents, ceramics, insulation, and chemical plants.

Searles Lake in California is a classic example. The total value of chemicals produced there has historically exceeded $1 billion. In the Atacama, nitrate deposits became world famous because extreme dryness preserved salts that wetter landscapes would have dissolved and dispersed. Quiet minerals, often. Big value, still.

Economic Value Does Not End With Extraction

Desert Sun as a Resource

Oil and minerals dominate the conversation, yet deserts also produce value from the surface itself. The U.S. Department of Energy notes that concentrating solar technologies perform best in arid regions with high DNI, or direct-normal irradiance. That makes many deserts energy landscapes twice over: fossil and mineral wealth below ground, solar wealth above it.

Chile shows how that overlap can work. The Atacama has some of the world’s highest solar irradiance levels, and solar PV plus wind already provide more than 34% of Chile’s electricity generation. In simple terms, a desert can mine copper for the energy transition and also generate power for it. Few regions carry both roles so clearly.

Service Economies Around Desert Projects

Once a major desert resource province starts operating, value spreads into drilling services, explosives, machine maintenance, assay labs, construction, catering, road haulage, rail links, port handling, environmental monitoring, and training. The deposit gets the headline. The service economy keeps the district alive.

This matters for a simple reason: many desert mines and oilfields are remote. Workers need housing. Plants need spare parts. Ore needs roads, pipelines, slurry lines, conveyors, or ports. A rich deposit without service support stays stranded.

Livelihoods, Land Use, and Diversification

There is another side to desert value, a calmer one. The World Bank has pointed out that desert ecosystem goods are already being used for solar power and that arid regions also support tourism, agro-food chains, and other livelihood options. For a desert region, that means the smartest economy is often layered: extraction in one corridor, energy in another, tourism or adapted farming where the land allows it.

That layered model matters because mineral prices move in cycles. Oil does too. A desert economy with only one pillar can feel every market swing. A region with mining, solar, logistics, and local enterprise has more room to breathe.

What Decides the Real Economic Value of a Desert Deposit

- Ore Grade Or Reservoir Quality: High grade helps, but recovery rate matters just as much.

- Water Access: In deserts, water can become a cost center before production even starts.

- Energy Supply: Diesel, grid power, gas, or solar all change project cost.

- Distance To Processing And Ports: A mine 50 km from a port is not the same business as one 500 km inland.

- Processing Route: Beneficiation, leaching, smelting, refining, acid plants, and export terminals all add or limit value.

- Scale: Large deposits can absorb infrastructure costs more easily.

- Product Market: Fertilizer, battery chemicals, fuel, gemstones, and industrial salts each follow different price cycles.

So the phrase economic value of deserts should not be reduced to “there are minerals there.” A desert resource earns its value through geology, processing, infrastructure, and market access together. Miss one of those, and the value drops fast.

Why This Topic Matters for Understanding World Deserts

Deserts are often pictured as places of absence: little rain, sparse vegetation, long distances. Economically, the picture is the reverse. Many deserts are places of concentration. Hydrocarbons, metals, fertilizer minerals, nuclear fuel minerals, industrial salts, and solar energy all gather there in unusual density.

That is why the Arabian Desert, the Sahara, the Atacama, the Namib, and other arid regions matter so much in the global economy. They are not blank spaces on a map. They are production landscapes. Dry, exposed, technically demanding, and often very valuable.

Sources

- https://education.nationalgeographic.org/resource/desert/ (desert definition, land coverage, population, and Arabian Desert oil reserve context)

- https://pubs.usgs.gov/gip/deserts/minerals/ (how arid climates form and preserve mineral deposits in deserts)

- https://pubs.usgs.gov/periodicals/mcs2025/mcs2025-lithium.pdf (2024 lithium production and reserve figures, including Chile and Namibia)

- https://pubs.usgs.gov/periodicals/mcs2025/mcs2025-copper.pdf (2024 copper production and reserve figures, including Chile)

- https://pubs.usgs.gov/periodicals/mcs2025/mcs2025.pdf (phosphate production data and phosphorus-use notes)

- https://pubs.usgs.gov/myb/vol3/2020-21/myb3-2020-21-morocco.pdf (Morocco phosphate reserves, mining export share, and employment data)

- https://repositorio.uchile.cl/bitstream/handle/2250/169399/Nitrate_deposits.pdf?sequence=1 (Atacama hyperaridity and nitrate deposit geology)

- https://www.iea.org/reports/chile-2050-energy-transition-roadmap/executive-summary (Chile’s copper and lithium supply share, Atacama solar irradiance, and electricity mix)

- https://world-nuclear.org/information-library/country-profiles/countries-g-n/namibia (Namib Desert uranium context and Namibia’s share of world uranium mining capacity)

- https://world-nuclear.org/information-library/facts-and-figures/uranium-production-by-country (2024 uranium production by country, including Namibia)

- https://publications.opec.org/asb/about/2600 (world proved crude oil reserves at the end of 2024)

- https://documents1.worldbank.org/curated/en/184141468757218802/pdf/P1303430PID0Print00301201201330655114770.pdf (desert livelihoods, solar potential, and wider economic value in arid regions)